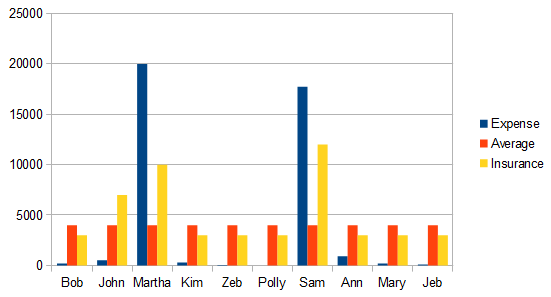

In this hypothetical example, 10 people had an average expense of $4,000 per some time unit (red). However, all but two were much lower than $4,000 and two, Martha and Sam, had much higher expense (blue). So this illustrates uncertainty--the driving idea of insurance. Of course the insurance company has its own expenses so say each person paid a bit higher than average, $5,000 per unit time, to the insurance company to cover these expenses (yellow). So the total expense paid out is $40,000 for all 10 people and the total payment to the insurance company is $50,000. (Of course this ignores insurance companies refusing to pay for things they said were covered when you bought the insurance. I have had plenty of experiences with that (refusing to pay the very thing that is in their booklet of covered expenses) but that is a different issue and for the moment lets just pretend the insurance company is honest and does what it says it will do--wouldn't that be nice⸮)

Now, say the insurance company has information about you. This could be anything, driving habits, medical, employment, credit rating, neighborhood you live in, ... The insurance company might then adjust your rates according to your predicted risk. This is good for the company, most people pay lower rates and the company will attract more of these lower risk people, but a few people pay higher rates based on risk factors. The company doesn't want to insure these people anyway and it would help the company if they went elsewhere for insurance. In the example above, the expenses and average is the same (a total expense of $40,000 for 10 people). The payment to the insurance company is the same (a total of $50,000), but there is a lower standard rate of $3,000 per person because some people pay a higher rate based on individual risks.

This is very good for the insurance company and on the surface it might seem fair to the consumers. Why should we all pay for a subset of people that choose risky lifestyles, etc. In fact it could be argued that this will actively encourage people to "clean up their act." But what if these risk factors are things people have no control over, like prior medical history or family history of a disease, etc. Also, in John's case above, he paid a higher rate but the company bet wrong; he actually had lower expenses for the period.

Now let's carry this to a ridiculous extreme to make a point. Say the insurance company had perfect predictive power; that they were able to essentially exactly predict the expense associated with each person over a long time period. What would the individuals expenses look like⸮

Above, the totals are exactly the same again, but the insurance payments are adjusted exactly according to each persons expense. Of course the company has its own internal expenses, so each person pays a bit more than their covered expense. In other words it would be better for all of these people to not have any insurance at all and just pay their own expenses. When the insurance company uses more and more information to reduce risk uncertainty, they are undermining the very reason for individuals to have insurance in the first place. There is no more shared risk and the people are just supporting a parasitic company for no benefit to themselves.

No comments:

Post a Comment